Introduction

Life insurance is one of the most important financial tools available for protecting families, preserving wealth, and creating financial security. Among the many types of life insurance available today, Term Life Insurance and Universal Life Insurance (UL) remain two of the most popular choices for consumers.

While both products provide a death benefit designed to protect loved ones, they serve very different purposes. Term life insurance is often chosen for its affordability and simplicity, while universal life insurance is valued for its flexibility, permanence, and potential cash value accumulation.

Understanding the differences between these two products is essential for making an informed financial decision. The right choice depends on your age, income, family situation, long-term financial goals, and budget.

This article explores how term life insurance works, how universal life insurance works, their advantages and disadvantages, and which type of policy may be best suited for different financial situations.

What Is Term Life Insurance?

Term life insurance is a form of life insurance that provides coverage for a specific period of time, known as the policy term. Common terms include:

- 10 years

- 15 years

- 20 years

- 30 years

- 35 years

If the insured dies during the policy term, the insurance company pays the death benefit to the policy beneficiaries. If the policyholder survives beyond the term period, coverage generally expires unless the policy is renewed or converted.

Because term insurance does not build cash value and provides temporary coverage, premiums are typically much lower than permanent life insurance products.

Key Features of Term Life Insurance

Affordable Premiums

One of the primary reasons consumers purchase term life insurance is affordability.

For example:

- A healthy 35-year-old may purchase a $500,000 term policy for a relatively low monthly premium.

- The same amount of permanent insurance could cost several times more.

This allows families to obtain significant protection during their highest financial obligation years.

Fixed Premiums

Most level term policies offer:

- Fixed premiums

- Fixed death benefits

- Guaranteed coverage periods

Premiums generally remain unchanged throughout the selected term.

Temporary Coverage

Coverage lasts only for the designated period.

Examples include:

- Protecting a mortgage

- Covering child-rearing years

- Income replacement during working years

- Business debt protection

Convertible Options

Many term policies include conversion privileges allowing policyholders to convert coverage into a permanent life insurance policy without additional medical underwriting.

Advantages of Term Life Insurance

1. Lowest Cost Protection

Term insurance offers the highest amount of death benefit per premium dollar.

Consumers can often purchase:

- $250,000

- $500,000

- $1 million

- $2 million+

of coverage at affordable rates.

2. Easy to Understand

Term policies are straightforward.

You pay premiums and receive coverage for a specific period.

There are no complicated cash value calculations or investment components.

3. Ideal for Income Protection

Many families depend heavily on one or two wage earners.

Term insurance can replace income and help cover:

- Mortgage payments

- College expenses

- Daily living expenses

- Outstanding debts

4. Flexible Coverage Amounts

Consumers can often purchase large amounts of protection while maintaining manageable premium costs.

Disadvantages of Term Life Insurance

1. Coverage Eventually Expires

The biggest drawback of term insurance is that it is temporary.

If coverage expires:

- New insurance may be more expensive

- Health conditions may make new coverage difficult to obtain

- Coverage may no longer be available

2. No Cash Value

Term policies generally do not accumulate savings.

There is:

- No investment account

- No policy loans

- No cash surrender value

The premiums pay solely for insurance protection.

3. Increasing Renewal Costs

Many policies allow annual renewal after the initial term.

However, renewal premiums often increase dramatically as the insured ages.

4. Potential for Outliving Coverage

Many policyholders live beyond their policy term and never receive benefits.

What Is Universal Life Insurance?

Universal Life Insurance (UL) is a permanent life insurance policy designed to provide lifetime coverage while also accumulating cash value.

Unlike term insurance, universal life combines:

- Death benefit protection

- Tax-advantaged cash value growth

- Premium flexibility

- Long-term planning opportunities

Universal life was introduced to give consumers greater flexibility than traditional whole life insurance.

Key Features of Universal Life Insurance

Permanent Coverage

Universal life insurance is intended to remain in force for the insured’s lifetime, provided policy requirements are met.

Coverage does not expire after:

- 10 years

- 20 years

- 30 years

as term insurance does.

Cash Value Accumulation

A portion of premium payments may accumulate as cash value.

Cash value may:

- Grow tax-deferred

- Be accessed through policy loans

- Be used for retirement income planning

- Help pay future premiums

Flexible Premiums

Universal life allows policyholders to adjust premium payments within policy guidelines.

This flexibility can help accommodate changing financial situations.

Adjustable Death Benefits

Many policies permit changes to the death benefit as financial needs evolve.

Types of Universal Life Insurance

Several variations of universal life insurance exist.

Traditional Universal Life

Cash value grows based on interest credited by the insurance company.

Generally provides:

- Conservative growth

- Stable accumulation

- Moderate risk

Indexed Universal Life (IUL)

Cash value growth is linked to a market index such as:

- S&P 500

- Nasdaq indexes

- Proprietary indexes

Policyholders receive upside potential with downside protection through policy guarantees.

Variable Universal Life (VUL)

Cash value is invested in subaccounts similar to mutual funds.

Potential advantages:

- Greater growth opportunity

Potential disadvantages:

- Market risk

- Investment losses

Guaranteed Universal Life (GUL)

Designed primarily for death benefit protection.

Typically offers:

- Minimal cash accumulation

- Lifetime guarantees

- Lower premiums than many other permanent policies

Advantages of Universal Life Insurance

1. Lifetime Protection

Coverage can remain in force throughout life.

This may be valuable for:

- Estate planning

- Legacy creation

- Wealth transfer

- Final expense protection

2. Tax-Advantaged Cash Value Growth

Cash value accumulates on a tax-deferred basis.

This means growth is generally not taxed annually.

3. Policy Loans

Policyholders may borrow against accumulated cash value.

Potential uses include:

- Retirement income

- Education funding

- Emergency expenses

- Business opportunities

4. Flexible Premium Structure

Universal life offers greater premium flexibility than many other permanent insurance products.

5. Estate Planning Benefits

Life insurance proceeds are generally income-tax-free to beneficiaries.

For affluent families, universal life can become a powerful estate planning tool.

Disadvantages of Universal Life Insurance

1. Higher Premiums

Permanent coverage costs significantly more than term insurance.

Consumers must commit to larger premium obligations.

2. Greater Complexity

Universal life policies contain:

- Cash value calculations

- Cost-of-insurance charges

- Crediting rates

- Policy illustrations

Many consumers require professional guidance to fully understand policy mechanics.

3. Performance Risk

Some UL products depend partly on:

- Interest rates

- Index performance

- Investment returns

Poor performance may require additional premiums.

4. Long-Term Commitment

Permanent insurance generally works best when maintained for many years.

Early surrender can reduce benefits and may involve surrender charges.

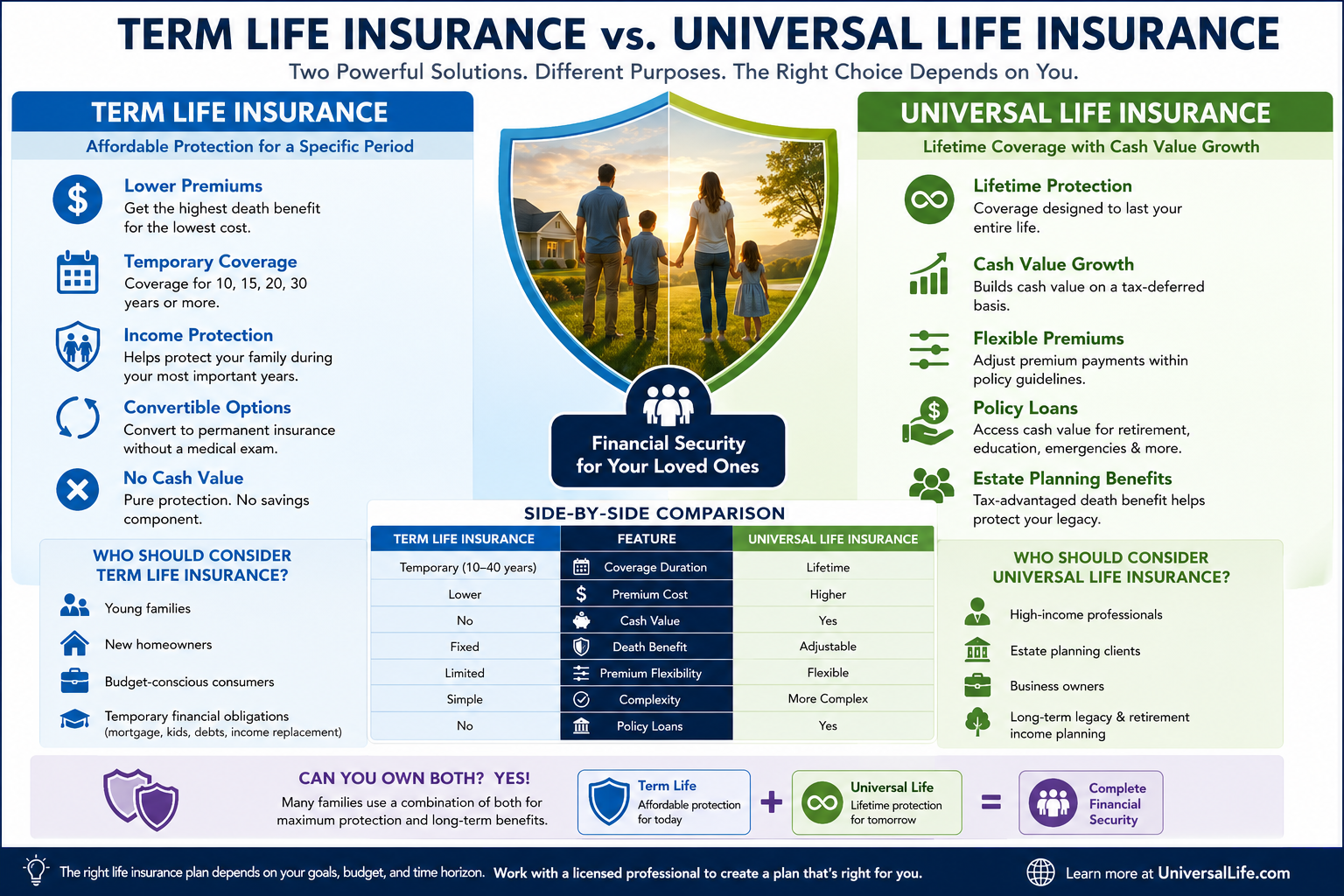

Side-by-Side Comparison

| Feature | Term Life Insurance | Universal Life Insurance |

|---|---|---|

| Coverage Duration | Temporary | Permanent |

| Premium Cost | Lower | Higher |

| Cash Value | No | Yes |

| Lifetime Coverage | No | Yes |

| Premium Flexibility | Limited | Flexible |

| Death Benefit | Fixed | Adjustable |

| Complexity | Simple | More Complex |

| Investment Component | None | Possible |

| Policy Loans | No | Yes |

| Estate Planning Use | Limited | Significant |

Who Should Consider Term Life Insurance?

Term insurance is often ideal for individuals who need maximum protection at minimum cost.

Examples include:

Young Families

Parents with children often require substantial income replacement protection.

New Homeowners

Mortgage obligations create a significant financial burden that term insurance can help protect.

Budget-Conscious Consumers

Individuals prioritizing affordable protection may find term insurance highly attractive.

Temporary Financial Obligations

Coverage may be needed only during:

- Working years

- Debt repayment periods

- Children’s dependency years

Who Should Consider Universal Life Insurance?

Universal life may be better suited for consumers seeking long-term financial planning benefits.

Examples include:

High-Income Professionals

Individuals looking for tax-advantaged accumulation opportunities.

Estate Planning Clients

Families wishing to transfer wealth efficiently.

Business Owners

Business succession planning often utilizes permanent life insurance.

Long-Term Legacy Planning

Individuals wanting to leave an inheritance regardless of when death occurs.

Retirement Income Strategies

Certain UL products may supplement retirement income through policy loans and withdrawals.

Can You Own Both?

Absolutely.

Many financial advisors recommend combining both products.

This strategy is sometimes called layering coverage.

Example:

- $1,000,000 30-year term policy

- $250,000 permanent universal life policy

Benefits include:

- Affordable protection today

- Lifetime coverage for future needs

- Cash value accumulation

- Estate planning benefits

This blended approach often provides an effective balance between affordability and permanence.

Common Consumer Questions

Is Term Insurance Better Than Universal Life?

Neither product is universally better.

The better choice depends on:

- Financial goals

- Budget

- Time horizon

- Family obligations

- Estate planning objectives

Can Term Insurance Be Converted?

Many policies allow conversion to permanent insurance without additional medical exams.

This can be valuable if health changes occur later.

Does Universal Life Always Build Cash Value?

Most universal life policies are designed to accumulate cash value, although growth varies depending on policy structure and performance.

Which Product Has Better Return on Investment?

Life insurance should first be viewed as protection rather than an investment.

However:

- Term insurance generally provides greater death benefit value per premium dollar.

- Universal life may provide long-term accumulation and planning benefits unavailable with term coverage.

The Bottom Line

Term Life Insurance and Universal Life Insurance each serve important but different roles in a comprehensive financial plan.

Term Life Insurance offers affordable, straightforward protection for a specific period and is often ideal for income replacement, debt protection, and family security during working years.

Universal Life Insurance provides permanent coverage, cash value accumulation, premium flexibility, and long-term wealth planning opportunities. It can be an effective solution for estate planning, retirement strategies, and creating a lasting financial legacy.

For many families, the best answer is not necessarily choosing one over the other. Instead, combining both products can provide substantial protection today while creating long-term financial security for tomorrow.

Before purchasing any life insurance policy, consumers should evaluate their financial objectives, coverage needs, risk tolerance, and long-term planning goals. Working with a licensed insurance professional can help determine the most appropriate strategy and ensure that life insurance aligns with an overall financial plan.