Universal life insurance is one of the most flexible and powerful forms of permanent life insurance available today. Unlike term life insurance, which provides coverage for a specific number of years, universal life insurance is designed to provide lifelong protection while also building cash value over time. For individuals and families seeking long-term financial security, tax-advantaged growth, and flexible premium options, universal life insurance can be an attractive financial planning tool.

In today’s evolving financial environment, many consumers are looking for insurance products that offer more than just a death benefit. They want flexibility, wealth accumulation opportunities, and protection against uncertainty. Universal life insurance was created to meet those needs by combining permanent life insurance protection with a savings component that can grow throughout the life of the policy.

This guide explains what universal life insurance is, how it works, its advantages and disadvantages, the different types available, and who may benefit most from owning a policy.

Understanding Universal Life Insurance

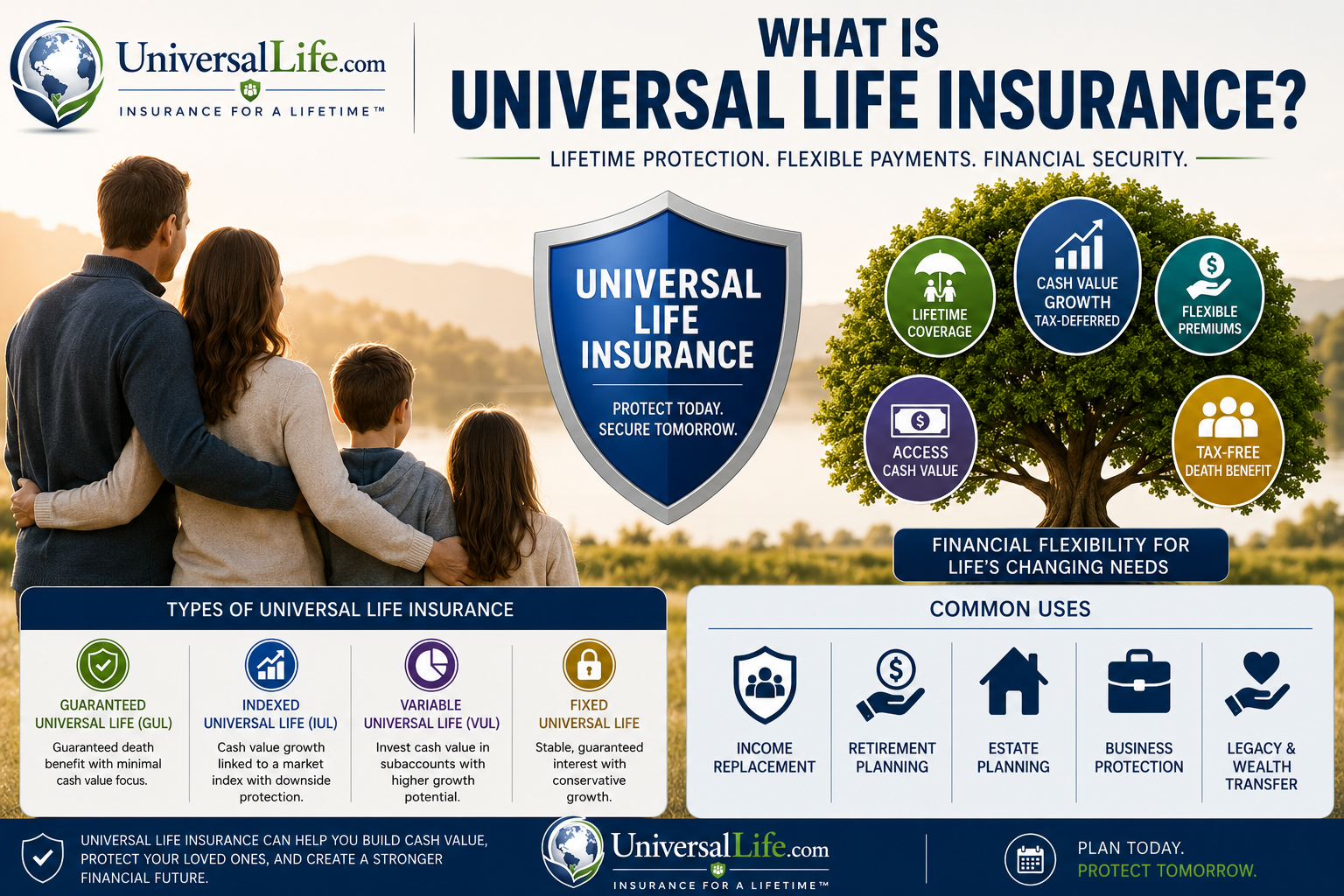

Universal life insurance (UL) is a type of permanent life insurance that provides:

- Lifelong coverage

- A death benefit for beneficiaries

- A cash value account that grows over time

- Flexible premium payments

- Adjustable death benefits in many cases

Unlike traditional whole life insurance, universal life insurance allows policyholders to adjust their premiums and death benefit within certain limits. This flexibility is one of the key reasons many consumers choose UL policies for long-term financial planning.

A portion of each premium payment goes toward the cost of insurance and administrative expenses, while the remaining amount is deposited into the policy’s cash value account. Over time, the cash value can accumulate and earn interest or investment-related returns depending on the type of policy.

How Universal Life Insurance Works

Universal life insurance operates differently from both term life and whole life insurance.

Premium Payments

One of the defining features of universal life insurance is premium flexibility. Policyholders can often:

- Increase or decrease premium payments

- Skip payments if enough cash value exists

- Pay additional premiums to grow cash value faster

This flexibility can be valuable during changing financial circumstances.

For example:

- During strong earning years, a policyholder may contribute extra funds to accelerate cash value growth.

- During difficult financial periods, the accumulated cash value may help cover policy costs temporarily.

However, flexibility must be managed carefully. Underfunding a universal life policy can cause the cash value to decline and potentially lead to policy lapse.

The Death Benefit

The death benefit is the amount paid to beneficiaries when the insured person dies.

Universal life insurance typically offers two main death benefit options:

Level Death Benefit

Also called Option A, this provides a fixed death benefit throughout the policy.

Example:

- $500,000 death benefit remains constant

As cash value grows, the insurance company’s risk decreases because the insurer subtracts the cash value portion from the amount at risk.

Increasing Death Benefit

Also called Option B, this combines:

- The base death benefit

- Plus accumulated cash value

Example:

- $500,000 base death benefit

- $100,000 cash value

- Total payout = $600,000

This option generally costs more because the insurer’s risk remains higher over time.

Cash Value Growth

One of the biggest attractions of universal life insurance is its cash value component.

The cash value grows tax-deferred, meaning policyholders generally do not pay taxes on gains while the funds remain inside the policy.

Depending on the policy type, growth may come from:

- Fixed interest rates

- Market index performance

- Investment subaccounts

The cash value can potentially be used for:

- Retirement income

- Emergency expenses

- College funding

- Business opportunities

- Estate planning

- Policy loans

Types of Universal Life Insurance

There are several forms of universal life insurance, each designed for different financial goals and risk tolerances.

1. Guaranteed Universal Life Insurance (GUL)

Guaranteed universal life focuses primarily on providing a guaranteed death benefit with minimal emphasis on cash value growth.

Features include:

- Lower premiums than whole life

- Guaranteed coverage to a certain age (often 90, 100, or 121)

- Limited cash value accumulation

- Greater stability

This type is often used for:

- Estate planning

- Income replacement

- Final expense planning

- Long-term family protection

GUL is popular among individuals who want permanent protection without investment risk.

2. Indexed Universal Life Insurance (IUL)

Indexed universal life insurance ties cash value growth to a stock market index such as the S&P 500.

Important features:

- Potential for higher returns

- Downside protection through minimum guarantees

- Growth caps and participation rates

- Tax-advantaged accumulation

IUL policies have become increasingly popular because they provide exposure to market growth without directly investing in the market.

For example:

- If the market index rises 10%, the policy may receive a portion of that gain.

- If the market declines, the policy may receive a 0% floor instead of losing value.

This balance of growth potential and protection is appealing to many long-term savers.

3. Variable Universal Life Insurance (VUL)

Variable universal life insurance allows policyholders to invest cash value directly into investment subaccounts similar to mutual funds.

Features include:

- Highest growth potential

- Greater investment control

- Higher risk exposure

- Market volatility

Unlike indexed UL, VUL policies can lose value if investments perform poorly.

These policies are often used by:

- Higher-income individuals

- Aggressive investors

- Advanced estate planners

Because of the investment risk and complexity, VUL policies require active management and financial knowledge.

4. Fixed Universal Life Insurance

Fixed universal life provides stable interest earnings determined by the insurance company.

Features include:

- Conservative growth

- Guaranteed minimum interest rates

- Lower risk

- Predictable performance

This type is appropriate for individuals prioritizing safety and stability over aggressive growth.

Universal Life Insurance vs. Term Life Insurance

Many consumers compare universal life insurance with term life insurance.

Term Life Insurance

Term life insurance provides coverage for a fixed period such as:

- 10 years

- 20 years

- 30 years

Advantages:

- Lower initial premiums

- Simple structure

- Strong temporary protection

Disadvantages:

- Coverage eventually expires

- No cash value accumulation

- Premiums increase with age upon renewal

Term life is often ideal for:

- Young families

- Mortgage protection

- Temporary income replacement

Universal Life Insurance

Universal life provides:

- Permanent coverage

- Cash value accumulation

- Flexible premiums

- Long-term planning opportunities

Advantages:

- Lifelong protection

- Tax-deferred growth

- Potential retirement income

- Estate planning benefits

Disadvantages:

- Higher costs

- Greater complexity

- Potential lapse risk if underfunded

UL is generally better suited for individuals seeking long-term wealth preservation and financial flexibility.

Universal Life Insurance vs. Whole Life Insurance

Whole life insurance and universal life insurance are both permanent policies, but they operate differently.

Whole Life Insurance

Whole life policies offer:

- Fixed premiums

- Guaranteed cash value growth

- Guaranteed death benefit

- Dividend potential in participating policies

Whole life emphasizes predictability and guarantees.

Universal Life Insurance

Universal life emphasizes:

- Flexibility

- Adjustable premiums

- Adjustable death benefits

- Potentially higher growth opportunities

UL policies generally require more active monitoring than whole life policies.

Advantages of Universal Life Insurance

Universal life insurance offers several significant benefits.

1. Lifetime Coverage

As long as policy requirements are met, coverage can remain in force for life.

This can help:

- Protect dependents

- Preserve wealth

- Cover estate taxes

- Fund legacy planning

2. Flexible Premiums

Policyholders can adjust payments based on:

- Income changes

- Financial goals

- Market conditions

- Retirement planning

This flexibility provides valuable financial adaptability.

3. Tax-Deferred Cash Value Growth

Cash value generally grows without current taxation.

This allows:

- Compound growth potential

- Efficient wealth accumulation

- Supplemental retirement income planning

4. Tax-Free Death Benefit

In most cases, beneficiaries receive the death benefit income-tax free.

This can provide:

- Immediate liquidity

- Debt protection

- Family financial stability

5. Access to Cash Value

Policyholders may access cash value through:

- Loans

- Withdrawals

- Partial surrenders

This creates financial flexibility during emergencies or retirement.

6. Potential for Market-Linked Growth

Indexed and variable UL policies may offer stronger long-term growth potential compared to traditional savings products.

Disadvantages of Universal Life Insurance

Despite its advantages, universal life insurance is not ideal for everyone.

1. Complexity

UL policies can be difficult to understand due to:

- Interest crediting methods

- Insurance costs

- Policy charges

- Market-related variables

Professional guidance is often recommended.

2. Risk of Policy Lapse

If premiums are insufficient and cash value declines, the policy may lapse.

This is especially important in:

- Underperforming indexed policies

- Rising insurance cost environments

- Aggressive loan scenarios

3. Higher Costs Than Term Insurance

Universal life premiums are significantly higher than term life premiums.

Consumers seeking only basic death benefit protection may find term insurance more affordable.

4. Variable Performance

Certain UL products depend heavily on:

- Interest rates

- Market conditions

- Policy funding strategies

Returns are not always guaranteed.

Who Should Consider Universal Life Insurance?

Universal life insurance may be appropriate for:

Families Seeking Long-Term Protection

UL policies can provide:

- Lifelong security

- Income replacement

- Legacy planning

High-Income Earners

High earners often use UL policies for:

- Tax-advantaged accumulation

- Supplemental retirement income

- Estate planning

Business Owners

Business owners may use UL policies for:

- Buy-sell agreements

- Executive compensation

- Key person insurance

- Business succession planning

Estate Planning Needs

UL insurance can help:

- Cover estate taxes

- Transfer wealth efficiently

- Equalize inheritances

Retirement Planning

Some individuals use properly structured UL policies as:

- Supplemental retirement vehicles

- Tax-efficient income sources

Policy loans can potentially provide tax-advantaged retirement distributions if managed correctly.

How Cash Value Loans Work

One major attraction of universal life insurance is borrowing against accumulated cash value.

Policy Loans

Policyholders can borrow funds from the insurer using the cash value as collateral.

Benefits:

- No credit check

- Flexible repayment

- Tax advantages in many situations

However:

- Interest accrues

- Excessive loans can reduce the death benefit

- Unpaid loans may trigger policy lapse

Proper management is critical.

Factors Affecting Universal Life Insurance Costs

Several factors influence premiums.

Age

Younger applicants generally receive lower rates.

Health

Medical history strongly impacts pricing.

Gender

Women often receive lower premiums due to longer life expectancy.

Tobacco Use

Smoking significantly increases costs.

Coverage Amount

Larger death benefits require higher premiums.

Policy Type

Indexed and variable UL policies may involve different pricing structures.

The Importance of Proper Policy Funding

One of the most misunderstood aspects of universal life insurance is policy funding.

Underfunding can create serious problems later because insurance costs increase with age.

Properly funded policies generally:

- Build stronger cash value

- Maintain long-term stability

- Reduce lapse risk

Many financial professionals recommend regular policy reviews to ensure performance remains aligned with expectations.

Common Uses for Universal Life Insurance

Universal life insurance serves many purposes beyond death protection.

Income Replacement

Provides financial support for surviving family members.

Wealth Transfer

Helps transfer assets efficiently to heirs.

Estate Liquidity

Can help pay estate taxes and expenses.

Business Protection

Protects companies from financial losses tied to key personnel.

Retirement Supplementation

Provides tax-advantaged income opportunities.

Charitable Giving

Can support philanthropic legacy planning.

Is Universal Life Insurance a Good Investment?

Universal life insurance is primarily an insurance product, not a pure investment vehicle.

However, it can provide:

- Tax advantages

- Conservative growth

- Wealth transfer benefits

- Long-term financial flexibility

Its value depends heavily on:

- Proper policy design

- Funding strategy

- Long-term objectives

Consumers seeking only investment returns may prefer traditional investment accounts. But for those seeking combined insurance protection and financial planning flexibility, UL can be highly valuable.

Questions to Ask Before Buying Universal Life Insurance

Before purchasing a policy, consumers should ask:

- What type of UL policy best fits my goals?

- How much flexibility do I need?

- What are the long-term costs?

- What assumptions are used in projections?

- How strong is the insurance company?

- What happens if returns are lower than expected?

- How will loans affect the policy?

Understanding these factors is essential for making an informed decision.

Choosing the Right Insurance Company

Not all universal life insurance policies are equal.

When comparing insurers, consider:

- Financial strength ratings

- Product performance history

- Policy fees

- Customer service

- Flexibility options

- Long-term stability

Top-rated insurers often provide stronger long-term reliability and policy support.

Final Thoughts

Universal life insurance remains one of the most versatile and customizable forms of permanent life insurance available. Its combination of lifelong protection, flexible premiums, tax-advantaged cash value growth, and estate planning benefits makes it an attractive option for many individuals and families.

While universal life insurance can be more complex than term or whole life insurance, it offers unique financial planning opportunities that extend far beyond a traditional death benefit. Whether used for family protection, retirement income planning, business succession, or wealth transfer, a properly designed UL policy can become an important part of a long-term financial strategy.

However, success with universal life insurance depends on understanding how the policy works, funding it appropriately, and reviewing it regularly. Because every person’s financial goals are different, working with a knowledgeable insurance professional can help ensure the policy aligns with both current needs and future objectives.

For consumers seeking flexibility, permanent coverage, and long-term financial potential, universal life insurance continues to be one of the most powerful tools in modern financial planning.